[ad_1]

Quantitative Easing Explained: Main Talking Points

- With rates near zero, Fed risks another quantitative easing tool

Bank of Japan’s economic and financial returns fall after years of quantitative easing

Similarly, the European Central Bank has used Long-Term Refinancing Operations (LTROs) as a form of quantitative easing, but questions remain about its effectiveness

How Does Quantitative Easing Work?

Quantitative easing, or “QE” for short, is a monetary policy tool that central banks typically use to boost domestic economies when using more traditional methods. The central bank’s purchase of securities — mostly government bonds — from its member banks effectively increases the economy’s money supply.

As supply increases, the cost of money falls, making it cheaper for businesses to borrow money to expand. This has a similar effect as standard short-term rate cuts by central banks; but depending on what they buy, these efforts can significantly reduce the cost of long-term lending. This could affect home, auto and small business loans more directly.

The Federal Reserve Bank (FED) Quantitative Easing Policy

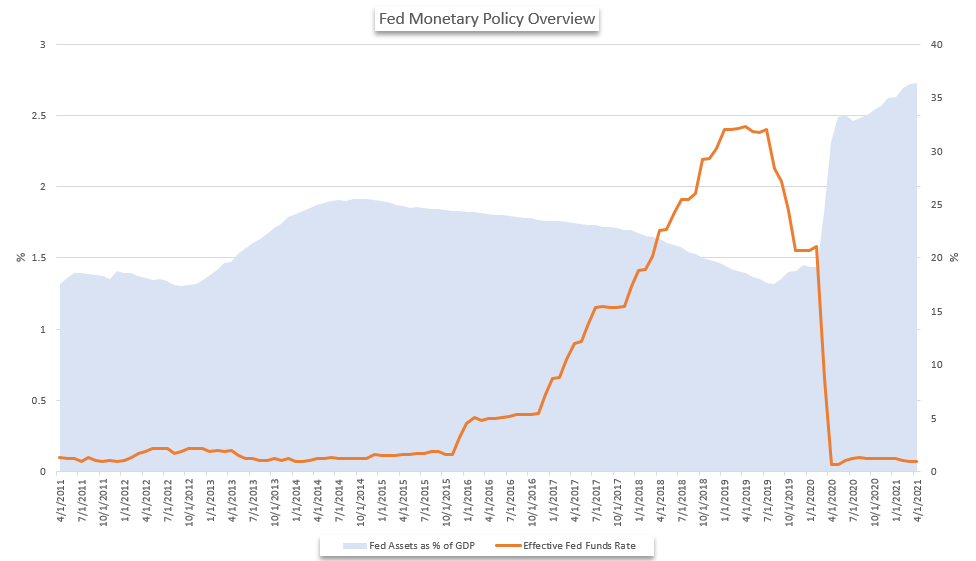

As the central bank of the United States, the Federal Reserve has the responsibility to provide the country with a more secure, flexible and stable monetary and financial system. This is often reduced to the twin mission of stabilizing inflation and low unemployment. To achieve these goals, the Federal Reserve is assigned a set of monetary policy tools that allow it to influence the dollar and the nation’s money supply. While raising and lowering the federal funds rate is the most well-known tool, central bank balance sheets have become increasingly under the radar and attention of investors.

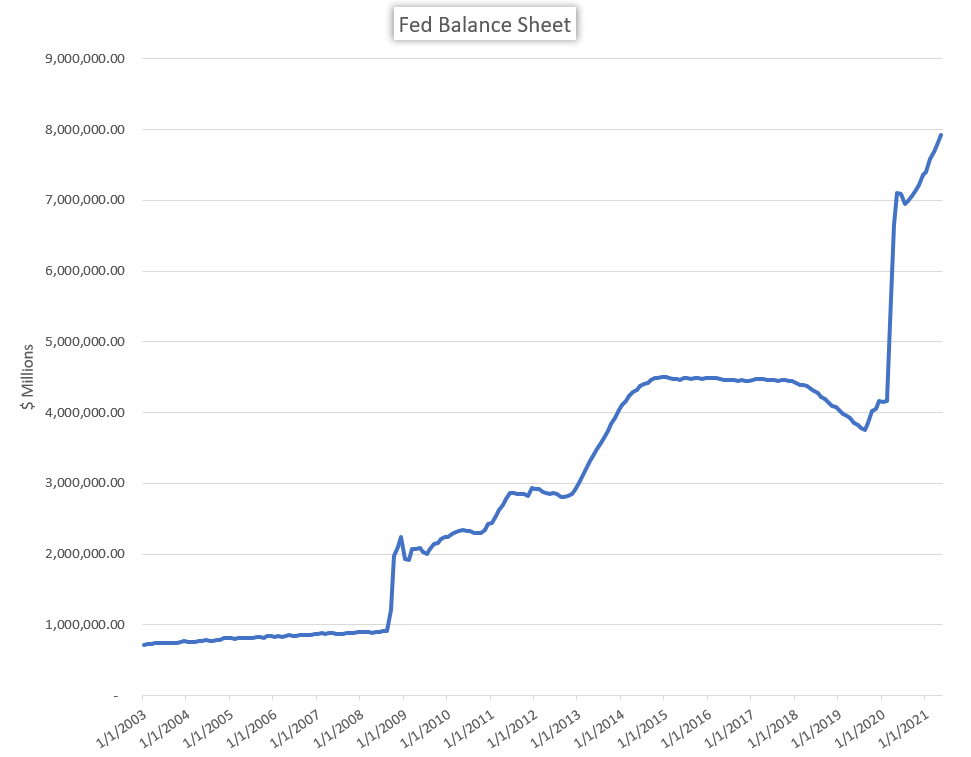

Federal Reserve Bank Total Assets

Source: FRED

Simply put, the Fed’s balance sheet is the same as any other. In the case of the Federal Reserve, the collection of various assets and liabilities is recorded at all Federal Reserve Bank branches. The Bank may use these assets and liabilities as unconventional or auxiliary monetary policy tools, especially when interest rates are already low and limit the potential for further monetary policy efforts.

When the U.S. economy fell into recession in 2008 due to the financial crisis, the Federal Reserve announced a series of rate cuts. As a typical expansionary tool, cuts are designed to stimulate spending, thereby improving the economy. But even with interest rates near zero, the economic recovery has not taken hold.

Then, in November 2008, the Federal Reserve announced its first round of quantitative easing, commonly known as QE1. The announcement caused the Fed to drastically alter its standard market operations and begin buying large quantities of Treasury bills, bills and bonds, as well as high-quality asset-backed and mortgage-backed securities. These purchases effectively increase the money supply in the U.S. economy and make it cheaper to obtain capital. The purchase program ran from December 2008 to March 2010 and was accompanied by a further reduction in the federal funds rate, resulting in a new interest rate range of 0% to 0.25%.

Change in Fed Balance Sheet due to Quantitative Easing

Source: Bloomberg

With the federal funds rate near zero at the time and reluctance to explore negative rates, the central bank used almost all of its accommodative monetary policy tools. As a result, quantitative easing has become an important tool for central banks to boost economic growth and repair the wreckage of the U.S. economy.

To further support the economic recovery, the Fed implemented subsequent rounds of quantitative easing, namely QE2 from November 2010 to June 2011 and QE3 from September 2012 to December 2013. The purchases targeted similar assets to help support expected U.S. growth — and capital markets as a spin-off — until the Fed finally reversed course when it first raised rates in December 2015.

Check out our free quarterly forecasts for USD, EUR, Dow Jones and more.

In 2019 we saw a debate on sustainable quantitative tightening (shortening of the balance sheet), after already starting to shrink the balance sheet in 2018. As the U.S. economy endures a decade of economic expansion, many Fed officials support the bank’s slow balance sheet reduction and advocate for further normalization. However, unbalanced growth and external risks such as trade wars complicate the issue of this particular support.

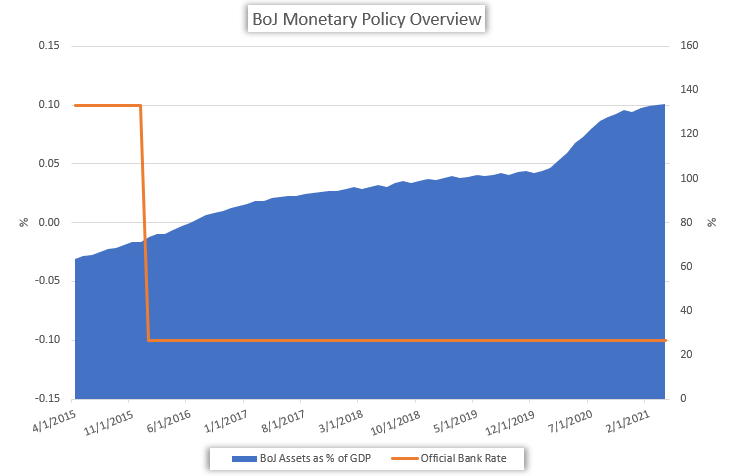

The Bank of Japan (BOJ) Quantitative Easing Policy

The Bank of Japan is another financial institution using quantitative easing, with mixed results. One of the earliest examples occurred between October 1997 and October 1998, when the Bank of Japan bought trillions of yen worth of commercial paper to help banks through slow growth, low interest rates and troubled bank lending. period. However, growth remains subdued.

Check our economic calendar for data releases and live event times.

From March 2001 to December 2004, in the face of a huge shock, the Bank of Japan stepped up its asset purchases. The round of purchases targeted long-term government bonds, injecting 35.5 trillion yen of liquidity into the Bank of Japan. While the purchases were modest, buying long-term government bonds dampened investment returns, and Japan’s growth faltered again as the Great Financial Crisis hit. Since then, the BOJ has implemented multiple rounds of quantitative easing and qualitative monetary easing (QQE), all of which have largely been ineffective as the country still struggles with low economic growth in a negative interest rate environment.

Source: Bloomberg

Today, the Bank of Japan has expanded into other forms of buying securities of different qualities. In addition to previous commercial paper purchases, the bank has also built a large stake in the country’s exchange-traded fund (ETF) market and in Japan’s real estate investment trusts (J-REITs).

Source: Bloomberg

The Bank of Japan started buying ETFs in 2010 and as of the second quarter of 2018 owned about 70% of the total ETF market in Japan. Additionally, these broad-based acquisitions make the Bank of Japan the majority shareholder in more than 40 percent of Japan’s listed companies, according to Bloomberg. As a result, the quality and creditworthiness of these assets held by the central bank is generally inferior to that of government-issued assets such as Japanese government bonds (JGBs), and differs significantly from those held by the Federal Reserve.

The Bank of England (BOE) Quantitative Easing Policy

Like the aforementioned central banks, the Bank of England has accumulated large amounts of local government bonds (GILTs) and corporate bonds through its own quantitative easing program. Policies to support the UK economy were adopted at the height of the global recession, which will eventually translate into increased political risk from a Scottish referendum, general election and ultimately Brexit. At the same time, banks have also slowly raised their notified currency rates.

Source: Bloomberg

The Bank of England’s total holdings are much smaller than those of its U.S. and Japanese counterparts. Compared to the country’s GDP, the Bank of England’s holding at the beginning of 2019 was only 5.7%, dwarfed by Japan’s holdings, which account for more than 100% of GDP. Relatively small holdings could allow banks to operate more efficiently in the future, as the drop in returns from quantitative easing has yet to take hold.

Source: Bloomberg

Currently, the effectiveness of the Bank of England’s quantitative easing strategy appears to have surpassed that of the Bank of Japan, in line with the Fed’s policy. With Brexit uncertainty lingering, the bank may decide to maintain its safety net and possibly even continue monetary policy action. However, the bank has made far less commitment to quantitative easing than its neighbor, the European Central Bank.

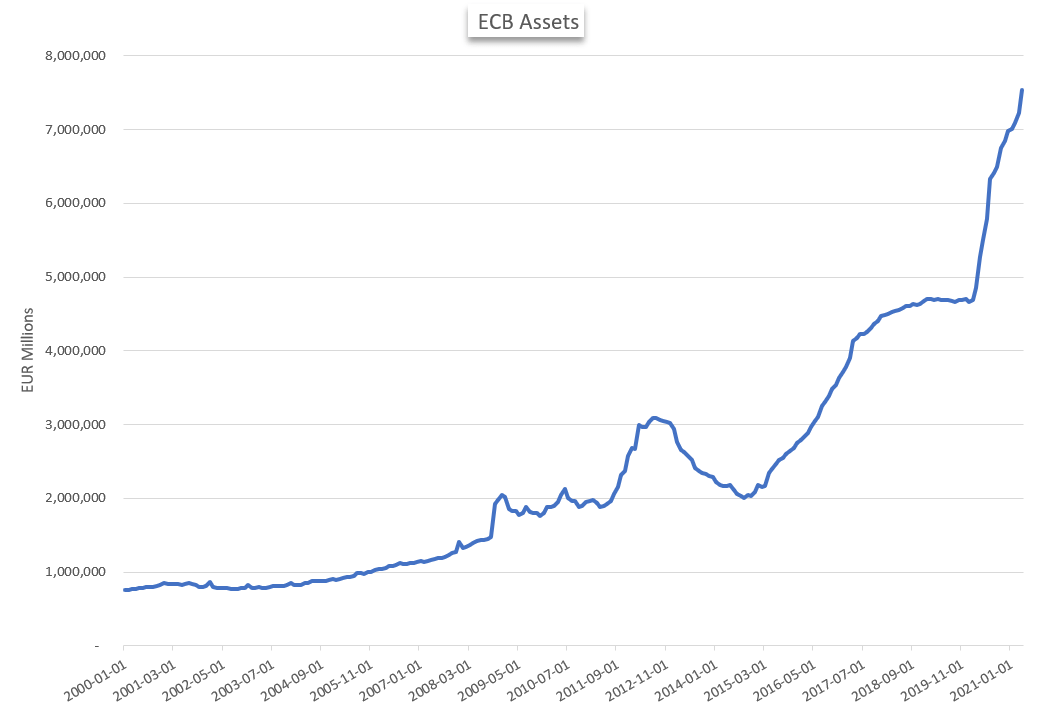

The European Central Bank (ECB) Quantitative Easing Policy

The ECB is another major central bank using QE as an expansionary tool – although it has been involved in traditional QE now significantly later than the Fed. In its latest round of easing, the ECB spent nearly $3 trillion buying government and corporate bonds, asset-backed securities and covered bonds.

The purchases were made between March 2015 and December 2018 to prevent sub-zero inflation from plaguing the European bloc, which is still recovering from the twin scourges of a global recession and the euro zone debt crisis. According to Reuters, the purchases were at 1.3 million euros per minute, which equates to 7,600 euros per person on the block.

Source: Bloomberg

As in Japan, several rounds of easing by the ECB have proven to be quite ineffective. In early 2019, months after its open-ended quantitative easing program ended, with interest rates remaining at zero, the bank announced another round of easing through targeted long-term refinancing operations (TLTROs). TLTROs inject low-rate money into euro zone banks to provide more bank liquidity and lower government bond yields. The loan term is one to four years.

Source: Bloomberg

TLTRO is designed to stabilize private banks’ balance sheets and their liquidity ratios. Stronger liquidity ratios make it easier for banks to lend, which reduces interest rates and should allow for inflation. However, years of monetary stimulus could lead to lower returns and adverse effects.

Negative Effects of QE: Balance Sheet Use and Diminishing Returns

While quantitative easing has been effective for the Fed and the US, monetary policy tools have been less effective and even had some negative effects on central banks in Japan and Europe. Years of expansionary policies have plunged Japan’s economy into deflation, and the bank’s balance sheet is now worth more than the country’s GDP.

Additionally, it may face greater risk in a downturn due to its large exposure to ETF, JRIET, and government bond markets. Despite multiple rounds of stimulus and negative interest rates, economic growth has not emerged and the Bank of Japan is entering a new realm of monetary policy.

Likewise, the ECB has found its own form of quantitative easing to have less of an impact on the European economy, as inflation and growth in the bloc remain subdued.

The Impact of Quantitative Easing on Currencies

Basically, the use of quantitative easing increases the supply of money. According to the prevailing principles of supply and demand, this change should cause the price of the currency to fall. However, since currencies are traded in pairs, the weakness of a currency is related to its counterpart.

Given the current monetary policy environment leaning towards tightening quotes and a dovish tone, few currencies have declared absolute strength. Recently, however, a quick best-of-breed mentality has gained strength, in which one central bank takes a dovish stance shortly after another. This delicate competition policy could become more aggressive and lead to so-called “currency wars”.

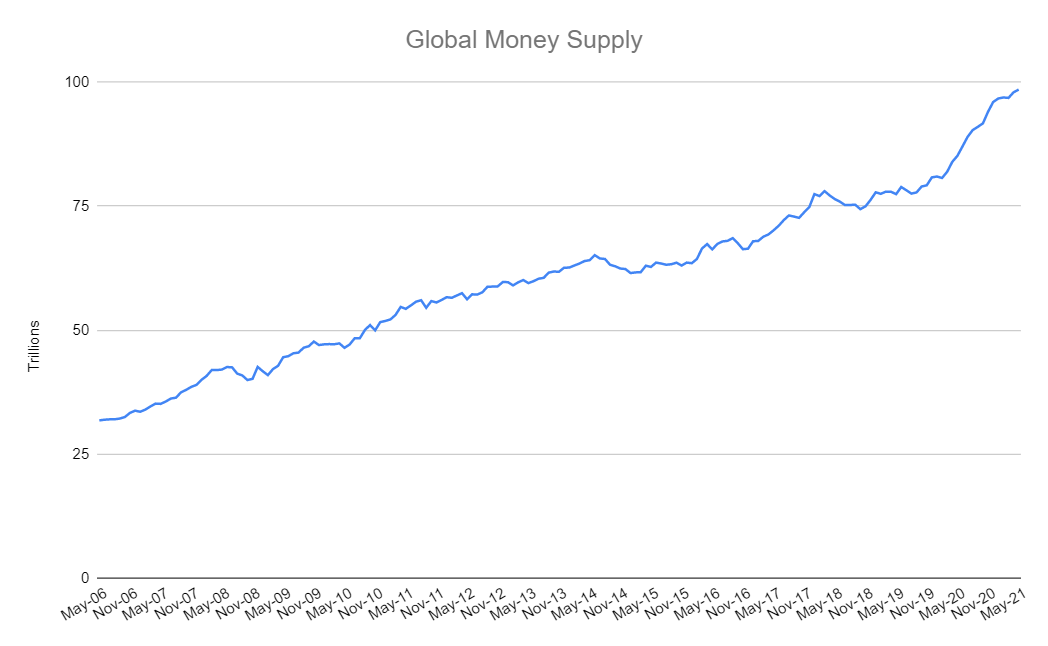

Source: Bloomberg

As a result, the global money supply has exploded while the relative value of currencies is still fluctuating. In the current monetary policy environment, the different approaches have largely become dovish comparisons. Few major central banks have imposed restrictions, and even fewer planned to raise interest rates. Instead, as quantitative easing appears to be gaining popularity as a monetary policy tool, officials have resorted to multiple rounds of capital injections — although it remains to be seen whether it will last.

Further reading on central banks and monetary policy

[ad_2]