[ad_1]

- Central banks look at various economic data and forecasts before making policies.

These data points are then applied to the central bank’s operational framework to determine if policy changes are needed.

To actually make policy, the central bank turns to the executive branch, which operates in the financial markets, to make policy.

How Central Banks Set Policy

Central bank policy is an important driver of financial market movements. Central bank officials collect, forecast and analyze economic data to determine the future path of the economy and its relationship to the bank’s policy goals. Challenges or deviations from the ideal economic process often prompt central banks to take monetary policy action. However, setting central bank policy is not as simple as issuing a press statement explaining interest rate changes, asset purchase adjustments or other support measures. Central bank policies must also be implemented through financial market transactions.

Central bank policies have direct and often direct effects on money markets. As central banks ease or tighten policy, holding their respective currencies is more or less attractive. Understanding the process by which central banks make such decisions is an invaluable skill for any trader.

Mandates and Price Stability

While the US Federal Reserve is the most watched and most important of the central banks, it’s mandate exceeds that of the average central bank. The Federal Reserve is dually focused on maximum employment and price stability, while most central banks are focused exclusively on the price stability mandate.

Price stability is best defined as low, stable, and predictable inflation. Most central bank’s target an inflation level of around 2%, which is viewed as a good indicator of strong and stable economic growth.

When making monetary policy decisions, central banks must weight a variety of economic indicators, expectations, and conditions.

Because being able to predict what central banks are likely to do will provide greater insight into any major economic data release.

Economic Data

Central banks analyze the same economic data that forex traders and other market participants closely monitor. Unemployment, housing and inflation are some of the key data points that central bankers track when they meet to discuss and formulate policy. These indicators are important to GDP and indicate growth or slowdown trends in major economies. The DailyFX Economic Calendar is a great tool that helps traders monitor the same data releases that central bankers keep a close eye on.

Recommended by Isaac Brooks

Trading Forex News: Strategies

Projections, Economists

In addition to tracking the same economic data available to market participants, the central bank employs hundreds of economists. These economists specialize in a specific area and are often seen as leaders in that area, making them the best candidates to be responsible for making forecasts that the central bank will use for policymaking. Economists forecast and model the future path of the economy based on current data, future expectations, their expertise and possible policy decisions.

Central bankers use these models to predict where the economy will go next and to assess the potential impact of their policy decisions. Many central banks regularly publish summaries of their economic and political forecasts, which are an invaluable resource for traders looking to understand how the market’s key drivers view the broader economy.

Framework

Once central banks have collected the required amount of economic data and forecasts, they apply it to the framework to determine if policy changes are needed. A central bank’s policy framework outlines its understanding of the relationship between key economic indicators and the central bank’s mandate, typically how a large number of economic data points will affect inflation.

The evolving world economy has led to an evolving central bank policy framework. Given the relationship between inflation and employment, monetary policymaking used to be based on simple rules and equations that dictated the appropriate level of interest rates. Since then, the world has become more complex, and central banks have moved away from this simplistic, rules-based approach to politics.

The most important development that has the greatest impact on central bank policy is the long-term trend towards low interest rates and low inflation in advanced economies.

Persistently low interest rates have diminished the ability of central banks to fight recessions by simply lowering interest rates. At the same time, despite a tight labor market and low interest rates, low inflation means central banks have had to reconsider and update their understanding of the relationship between employment and inflation

Given these changing trends, both the Federal Reserve and the European Central Bank have reviewed their monetary policy frameworks. While the ECB’s review and conclusions are still ongoing, the Federal Reserve announced its findings and new policy framework in late summer 2020. In that statement, Fed officials acknowledged that the relationship between inflation and employment had changed and that the economy could tolerate higher levels of employment without inflation being a threat. The Fed also changed its inflation policy from a symmetric target of 2% to an average target of 2%, which means that Fed policymakers will now tolerate inflation above 2% as long as higher inflation helps raise average inflation to 2%. 2%. Essentially, this new framework tells markets that the Fed will no longer seek to tighten monetary policy when there are signs of overheating, but instead allow monetary policy to remain accommodative and the economy to continue to heat up.

Once the central bank incorporates new economic data and forecasts into its framework, it makes a decision. While such decisions used to be as simple as raising or lowering interest rates, since the financial crisis, central banks’ toolboxes have expanded dramatically as they have taken a larger role in supporting the financial system and the wider economy.

Recommended by Isaac Brook

Forex for Beginners

Before the financial crisis, most central banks had relatively standardized tools. These central banks would set short-term interest rates and control bank lending through reserve requirements and other similar indicators. The main exception to these simple tools is the Bank of Japan, which has used “unconventional” monetary policy tools since the late 1990s, when Japan was struggling to emerge from a severe recession and deflation.

Learn about major financial bubbles, crises and flash crashes

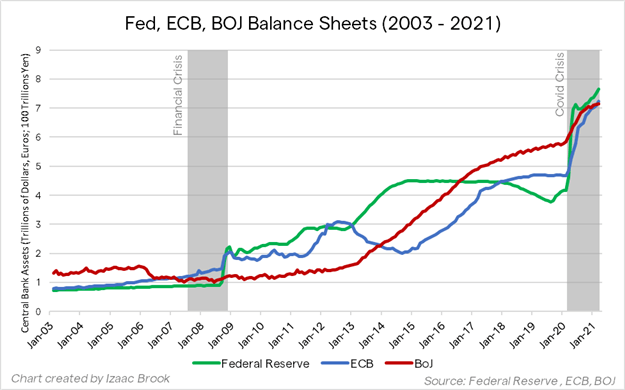

After the financial crisis, the global economy is in a state of shock. Global central banks, led by the Federal Reserve, began to pursue the same unconventional policies as the Bank of Japan. They bought a lot of government bonds, injected a lot of liquidity into the financial system, and lowered and kept interest rates at zero or even negative. During the crisis, central banks have also used their lending powers to create new, targeted instruments that can support key areas of the financial system, such as money market funds and large broker-dealers, that are not traditionally supported by central banks scope. tool.

These unconventional tools have become an important part of central bank toolkits and played a huge role during the Covid crisis. In addition to cutting interest rates to the zero lower bound, central banks have expanded their support measures beyond those seen during the financial crisis, pledging to support corporate bond markets, shore up key parts of the financial system and buy trillions of dollars in government bond bonds.

Recommended by Isaac Brook

Why is trust important?

Quantitative Easing

After the financial crisis, central banks began manipulating long-term interest rates to inject liquidity into the financial system to better support economic spending, growth and inflation. Through massive asset-purchase programs, better known as quantitative easing (QE), central banks have purchased large amounts of government bonds from the open market. Technically, these operations are similar to traditional open market operations conducted by central banks before the crisis, only on a much larger scale. While the exact mechanism by which quantitative easing works is still debated, such programs lower long-term interest rates, help support inflation, and often provide tailwinds to other financial markets.

Quantitative easing has also become increasingly important given the chronically low interest rates faced by advanced economies. During recessions, central banks are no longer able to easily lower interest rates to levels needed to stimulate the economy, and instead turn to more quantitative easing programs. Research shows that an asset purchase program of about 1.5% of GDP has a similar effect as a 25 basis point rate cut. With interest rates in the U.S. at just 1.50% prior to the Covid crisis, and even lower elsewhere, an ongoing program of quantitative easing should make up for traditional rate cuts. As a result, asset purchase programmes have soared since the onset of the Covid-19 crisis, pushing central bank balance sheets to record levels.

Implementation

These unconventional support measures are implemented by the central bank’s monetary policy executive department. In the executive sector, central bank policy is actually carried out through transactions and technical adjustments in financial markets. Policy decisions by senior central bankers are passed on to central bank dealers, who then trade with specific counterparties to change interest rates or otherwise make monetary policy decisions.

Rates Setting: Pre-Crisis

For the Fed, monetary policy is carried out through the Federal Reserve Bank of New York. Before the financial crisis, the decision on the federal funds rate was communicated to market traders. These dealers will conduct open market transactions with primary dealers.

Primary dealers are the primary banks that are approved as counterparties to the New York Fed, creating markets and supporting issuance of U.S. Treasuries. The New York Fed’s Markets Department will buy or sell a certain amount of U.S. Treasuries from these banks, adjust liquidity in the financial system, and push short-term interest rates into the range desired by the FOMC.

This fine-tuning of liquidity was a process used by central banks around the world before the unconventional tools of the financial crisis came into play. With the global financial system inundated with liquidity, policymaking has had to move beyond this basic approach.

Rates Setting: Post-Crisis

Following the central bank’s quantitative easing operations during the financial crisis, the impact of traditional open market operations on liquidity and credit conditions was insufficient to significantly tighten or ease interest rates. The Fed’s main policy lever has been the rate on reserves, the rate at which banks deposit “freshly printed” quantitative easing money directly at the Fed.

Visit our central bank calendar for interest rate decisions

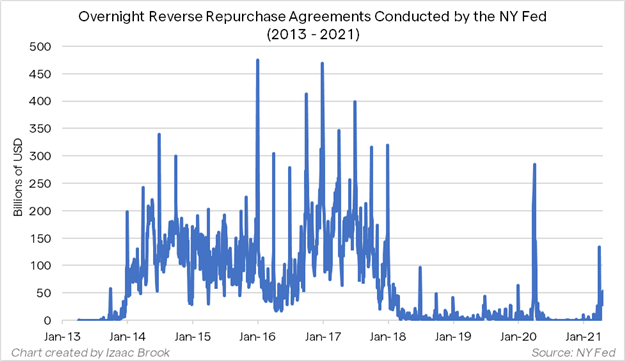

Activity in the federal funds market has plummeted as banks no longer need to seek capital to meet regulatory requirements and do not want to lend to other banks on an unsecured basis. Instead, interbank lending has moved to the repo market, where loans are secured by collateral. The New York Fed’s repo and reverse repo facilities have become important tools for managing excess liquidity in the system, and interest rates on these facilities are often adjusted in tandem with the Fed’s main policy rate.

The repurchase (RP) facility allows the Federal Reserve to provide Treasury collateral and capped-rate loans to market participants seeking funding. The reverse repo facility (RRP) is the opposite, in which the Fed lends Treasury collateral to market participants with excess cash. The RRP tool is used to temporarily withdraw reserves from the system and set a floor on interest rates.

In 2014-2018, the peak of the Fed’s balance sheet before the pandemic, the RRP facility shrank sharply at the end of the quarter as excess cash was withdrawn from the rest of the financial system, preventing interest rates from falling below the FOMC’s threshold. The lowest goal fell. In the post-pandemic world, with bank reserves hitting record highs, one should expect similarly heavy use of RRP tools at the end of the quarters ahead. The New York Fed raised the counterparty limit for the tool at its March 2021 FOMC meeting in preparation for future use.

Learn how central banks affect the foreign exchange market

Unconventional Policy Implementation

The quantitative easing program is implemented in the same way as open market operations. Traders in the central bank’s policy-enforcement arm issued announcements and timetables detailing their buying plans. Their counterparties submit a list of bonds they are willing to sell to the central bank, and central bank dealers select and trade the most competitive bids. While the internet is full of central bank-centric memes of printing money, the actual money central banks create in exchange for these bonds is just electronic money. Counterparty accounts are credited with the new digital currency from the central bank.

Communication is Key

Another important development in the central bank’s toolbox is forward guidance, given the evolution of monetary policy implementation since the financial crisis. Forward guidance is the communication of future interest rate developments. The premise of forward guidance is simple: companies, investors and markets are constantly trying to predict what the central bank will do next. By clearly communicating their plans, central bankers can adjust expectations to the desired point and bring greater clarity to markets. Forward guidance is linked to the monetary policy framework and applies the central bank’s view of key indicators to its communication of future policy.

Communication, transparency and setting expectations are an evolving part of central bank policy. Transparency in monetary policy helps central banks maintain predictability and credibility.

That’s a valuable metric for an institution with so much power over the financial system. The Federal Open Market Committee started using forward guidance in the wake of the financial crisis, saying rates would remain at zero “for some time.” As the recovery continued, forward guidance language evolved into a date-based approach and then an outcome-based approach. Both approaches help set long-term expectations for monetary policy and have proven useful to central banks around the world.

Central banks have reinstated forward guidance during the Covid crisis, providing markets with clear information on the outlook for interest rates, tapering expectations and the trajectory of asset purchase programmes. For its part, the Fed continued to stick to guidance consistent with its new framework despite strong economic data and inflation concerns. FOMC members reiterated that tapering and rate hikes won’t happen until significant progress is made on the Fed’s goals.

Hawks vs. Doves: How Monetary Policy Affects Forex Trading

Setting Policy, Summation

Central bank policy has changed significantly over the past two decades. While there has been no major change in the data the central bank tracks to set policy, the way policy is implemented has changed a lot. The development of long-term trends after the financial crisis has also created a need for new policy innovations. Central banks now control interest rates and monetary policy through liquidity management, large-scale asset purchases, technical adjustments in money markets, and improved communication. Understanding how these components interact and influence each other and how they affect the entire financial market is valuable knowledge for any trader.

— Written by DailyFX Research Intern Izaac Brook

[ad_2]