[ad_1]

How to Trade Geopolitical Risks

- Global economy shows growing weakness and vulnerability

Weak economic strength exposes markets to geopolitical risks

Examples of political threats in Asia, Latin America and EuropeCheck out our free guide on how to use economic news in your trading strategy!

ANALYZING GEOPOLITICAL RISKS

Against the backdrop of eroded fundamentals, markets are increasingly sensitive to political risks as their ability to trigger market volatility is amplified. Uncertainty-driven volatility tends to occur when liberal-leaning ideologies — namely free trade and integrated capital markets — are attacked by nationalist and populist movements around the world.

What makes political risk so dangerous and elusive is the limited ability of investors to price it. Therefore, traders may be taken aback if the global political landscape continues to develop unpredictably. Moreover, similar to the spread of the 2020 coronavirus, political pathogens may also have similar contagious effects.

In general, markets are not really political categories, but economic policies embedded in the agenda of who owns the sovereign.

Strategies aimed at stimulating economic growth tend to attract investors who want to park their money where they can earn the highest returns.

These include implementing stimulus packages, strengthening property rights, allowing the free flow of goods and capital, and removing regulations that hinder growth. If these policies generate enough inflationary pressures, central banks can raise interest rates in response. That increased the underlying yield on local assets, attracting investors and boosting the currency.

Conversely, a government with an underlying ideological bias against the globalization gradient could lead to capital flight. Regimes that try to tear apart the threads of economic and political integration often create uncertainty rifts that investors are reluctant to cross. Issues such as ultra-nationalism, protectionism and populism have often proven market disruptive.

When a country undergoes an ideological adjustment, traders will assess the situation to see if their risk/reward profile has changed fundamentally.

EUROPE: EUROSCEPTIC POPULISM IN ITALY

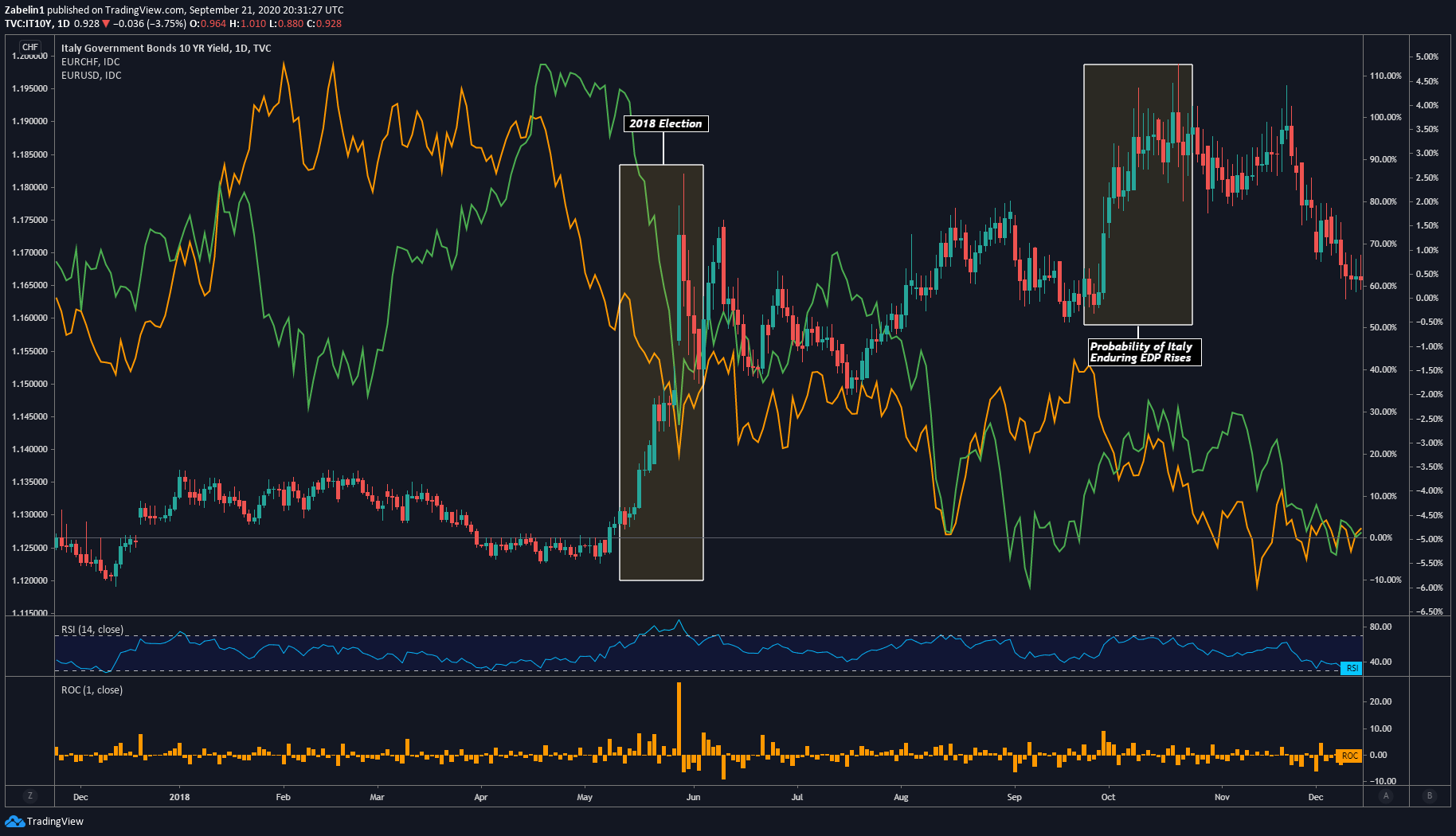

In Italy, the 2018 election shook regional markets and ultimately the entire financial system. The rise of the right-wing, anti-establishment Northern Alliance and the ideologically contradictory Five Star Movement was built on a populist movement fundamentally opposed to the status quo. Uncertainty associated with this new system was quickly factored into prices, resulting in wild swings.

The risk premium for holding Italian assets rose, reflected in a more than 100% rise in Italian 10-year bond yields. This suggests that if investors believe they are taking on more risk, they will demand higher returns. It was also reflected in the sharp widening of credit default swap spreads on Italian government bonds amid growing concerns that Italy could be at the heart of another EU debt crisis.

EUR/USD, EUR/CHF fall as Mediterranean government bond yields rise on fears of another euro zone debt crisis

Source: TradingView

The dollar, yen and Swiss franc all appreciated at the expense of the euro as investors shifted their funds to less risky assets. The euro’s troubles have been prolonged by a dispute between Rome and Brussels over the euro’s fiscal ambitions. The government’s fiscal privilege is a feature of its anti-establishment nature, which in turn leads to greater uncertainty, which in turn is reflected in a weaker euro.

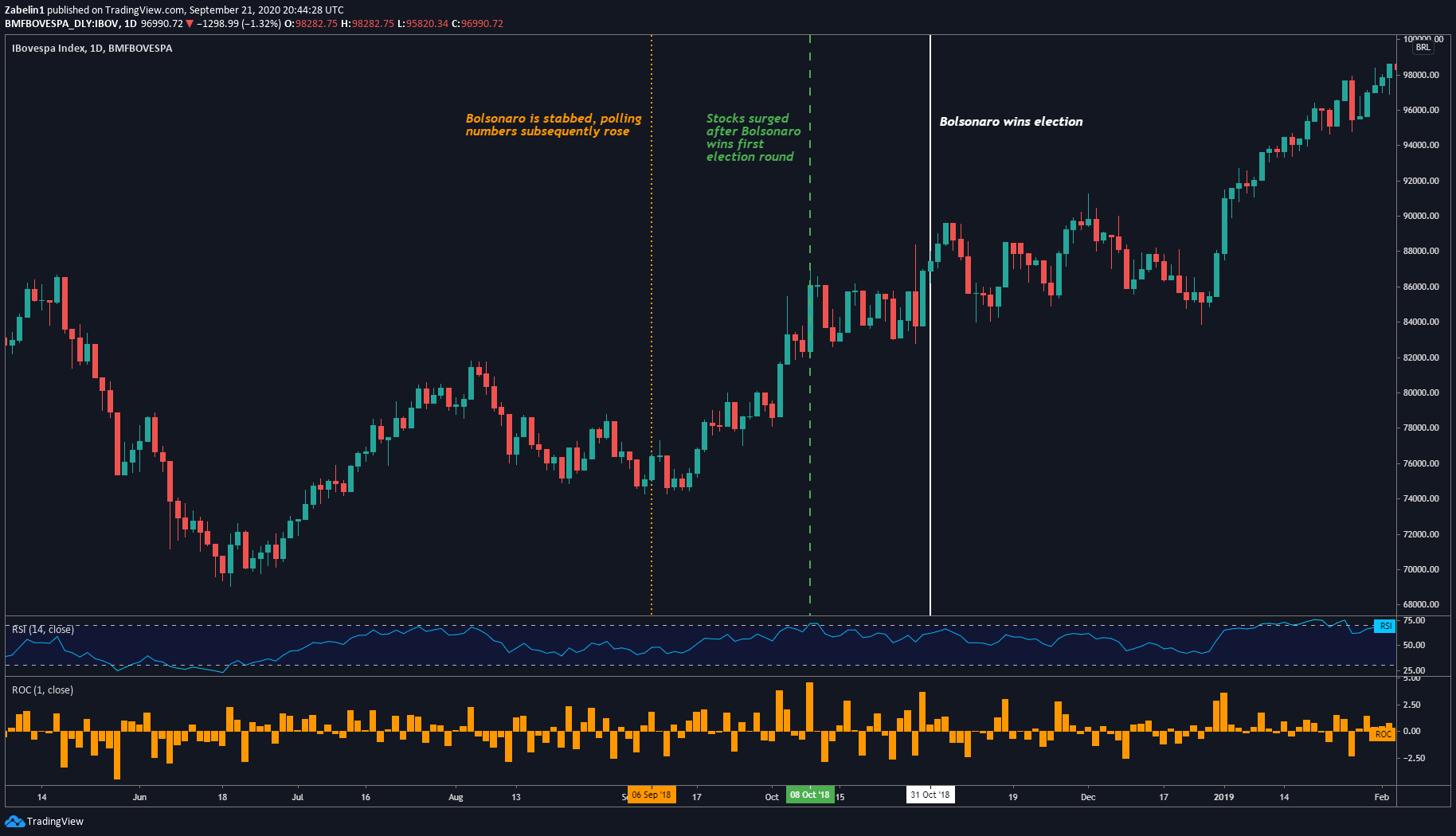

LATIN AMERICA: Nationalist-Populism in Brazil

Although President Jair Bolsonaro is often described as a brand nationalist with populist underpinnings, the market’s reaction to his rise to power has been welcomed by investors with open arms. His appointment of Paulo Guedes, a University of Chicago graduate economist with a passion for privatization and regulatory restructuring, has boosted investor sentiment and confidence in Brazilian assets.

Ibovespa index – daily chart

Source: TradingView

Between June 2018 and early 2020, when Covid-19 caused global markets to crash, the Ibovespa benchmark rose more than 58%, while the S&P 500 rose just over 17% over the same period. Brazil’s index rose more than 12 percent in just one month in October’s election, when polls suggested Bolsonaro would beat leftist rival Fernando Haddad.

The ups and downs in Brazil’s markets since Bolsonaro took office as president have mirrored his pension reform process. Investors speculate that these structural changes will be enough to lift Brazil’s economy out of the brink of recession and onto a path of robust growth unencumbered by unsustainable public spending.

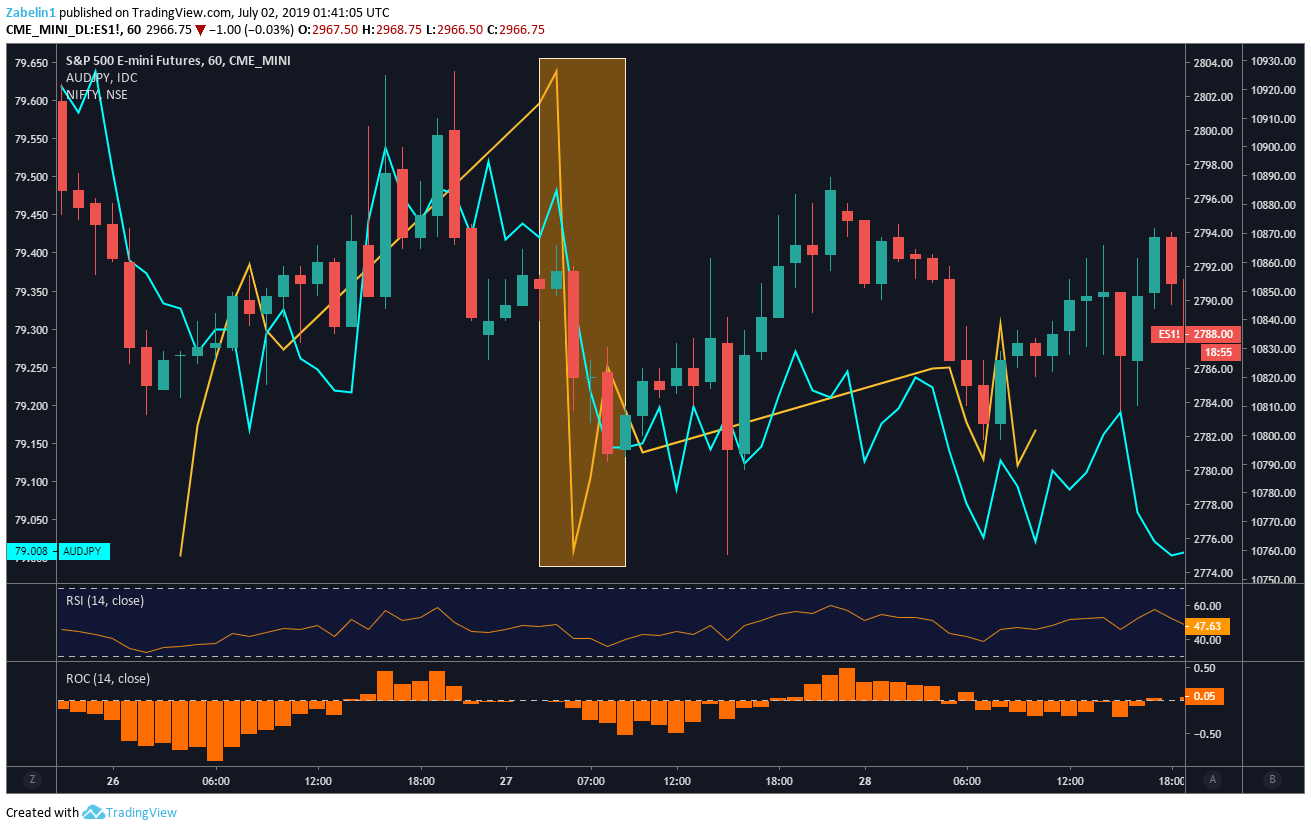

ASIA: Hindu Nationalism in India

Despite persistent concerns about the impact of Hindu nationalism on regional stability, the re-election of Indian Prime Minister Narendra Modi has been largely welcomed by the market. Modi, however, is known as a pro-business politician. His decision prompted investors to allocate large amounts of capital to Indian assets.

However, investor optimism has often been eroded by periodic clashes between India and its neighbors over territorial disputes. In early 2019, India-Pakistan relations deteriorated sharply following a skirmish in the disputed region of Kashmir. Hostility between the two nuclear powers has been a regional threat since their partition in 1947.

India Nifty 50, S&P 500 futures, AUD/JPY down on India-Pakistan conflict news

Source: TradingView

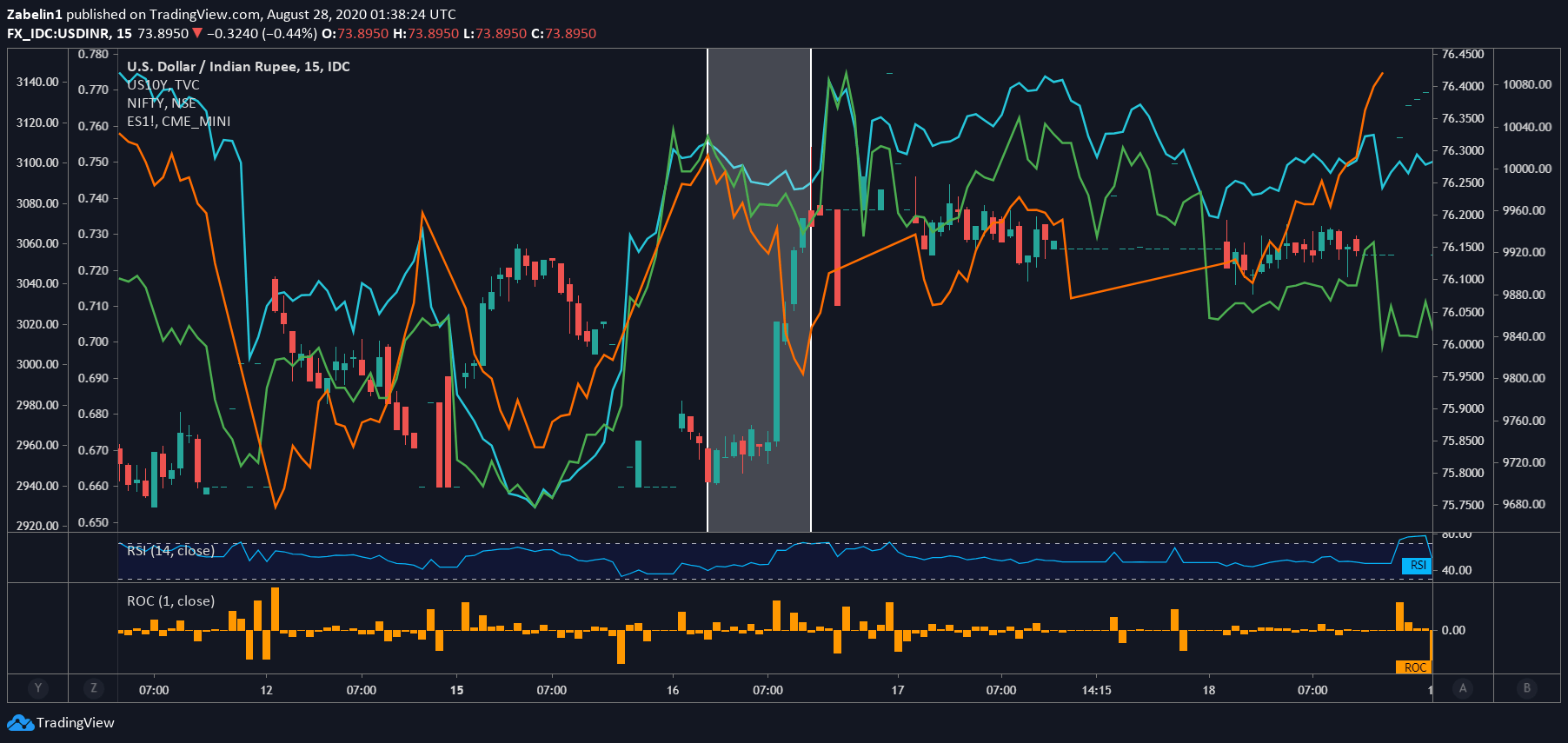

Tensions between India and China, especially along the disputed Himalayan border known as the Line of Actual Control (LAC), have also rattled Asian financial markets. In June 2020, news of a clash between Chinese and Indian troops that killed more than 20 people raised concerns about what further escalation could mean for regional security and financial stability. Read the full report here.

India Nifty 50, S&P 500 futures, US 10-year yield, USD/INR, after news of India-China conflict

Source: TradingView

Nationalist movements and governments involve political risk because the nature of such regimes is a show of strength, and compromise often equates to surrender. In times of political instability and economic fragility, the inherently recalcitrant nature of nationalist regimes can take longer to resolve disputes, compounding the financial impact of a diplomatic breakdown.

US Presidents Donald Trump and Modi have used similarly harsh rhetoric on the campaign trail and within their respective governments. Ironically, their ideological similarities could actually be a force for rupture in diplomatic relations. Tensions between the two countries escalated in 2019, with markets fearing that Washington could start another trade war in Asia and open a second front in India after already attacking China.

HOW FX REACTS AS GOVERNMENTS, CENTRAL BANKS RESPOND TO GEOPOLITICAL & ECONOMIC STRESS

For economies with high levels of capital liquidity, there are four main policy mix options that can trigger foreign exchange market reactions after economic or geopolitical shocks:

Scenario 1: Fiscal policy expands + monetary policy becomes tighter (“tightening”) = bullish for local currency

Scenario 2: Fiscal policy is already restrictive + monetary policy becomes more expansionary (“easy”) = bearish local currency

Scenario 3: Monetary Policy Expansion (“Easy”) + Fiscal Policy Tightening = Bearish Local Currency

Scenario 4: Monetary policy has tightened (“tightening”) + fiscal policy has become more expansionary = bullish local currency

It is important to note that for an economy like the US and a currency like the US dollar, whenever fiscal and monetary policy move in the same direction, it tends to have a vague effect on the economy

Scenario 1 – FISCAL POLICY LOOSE; MONETARY POLICY BECOMES TIGHTER

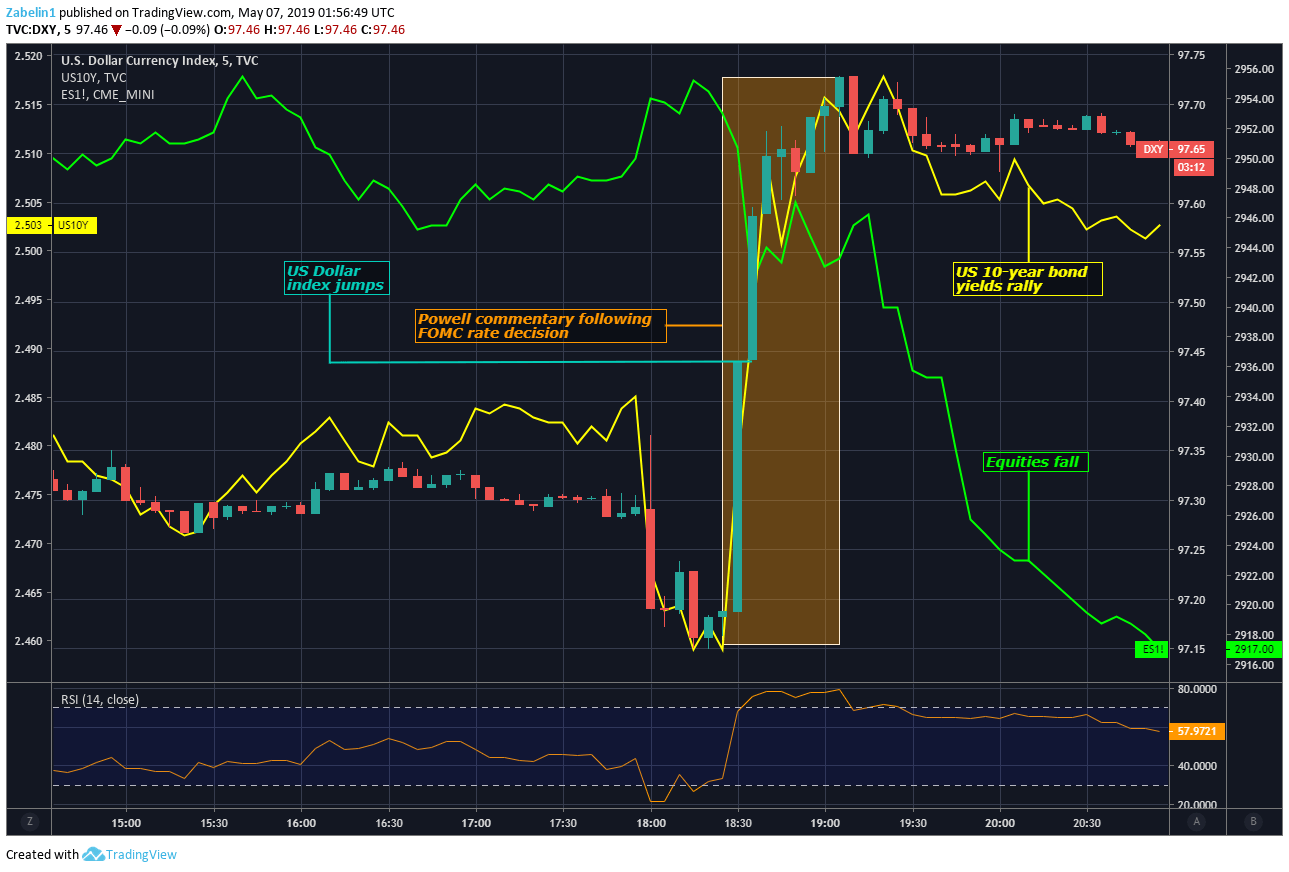

On May 2, 2019, following the FOMC’s decision to keep interest rates in a range of 2.25% to 2.50%, Fed Chairman Jerome Powell said that relatively weak inflation pressures at the time were “transitory.” This means that price growth, while slower than the central banker had expected, will soon accelerate. The U.S.-China trade war has played a role in slowing economic activity and curbing inflation.

The message implied at the time was a reduced chance of a short-term rate cut, as the fundamental outlook was seen as solid and the U.S. economy was on a generally healthy path. The neutral tone adopted by the Fed was less dovish than the market had expected. That could explain why the likelihood of the Fed cutting rates by the end of the year (as indicated by overnight index swaps) fell from 67.2% to 50.9% following Powell’s comments.

Meanwhile, the Congressional Budget Office (CBO) forecasts that the budget deficit will increase within three years, coinciding with a potential cycle of central bank tightening. Moreover, this comes amid speculation about a bipartisan stimulus package. In late April, key policymakers announced a $2 trillion infrastructure plan.

Recommended by Dimitri Zabelins

Improve your marketing with IG customer sentiment data

The combination of expansionary fiscal policy and monetary tightening suggests a bullish outlook for the dollar. The fiscal plan is expected to create jobs and boost inflation, prompting the Fed to raise interest rates. Coincidentally, the dollar gained an average of 6.2% against major currencies over the next four months.

Scenario 1: DXY, 10-year yields rise, S&P500 futures fall

Source: TradingView

Scenario 2 – FISCAL POLICY TIGHT; MONETARY POLICY BECOMES LOOSER

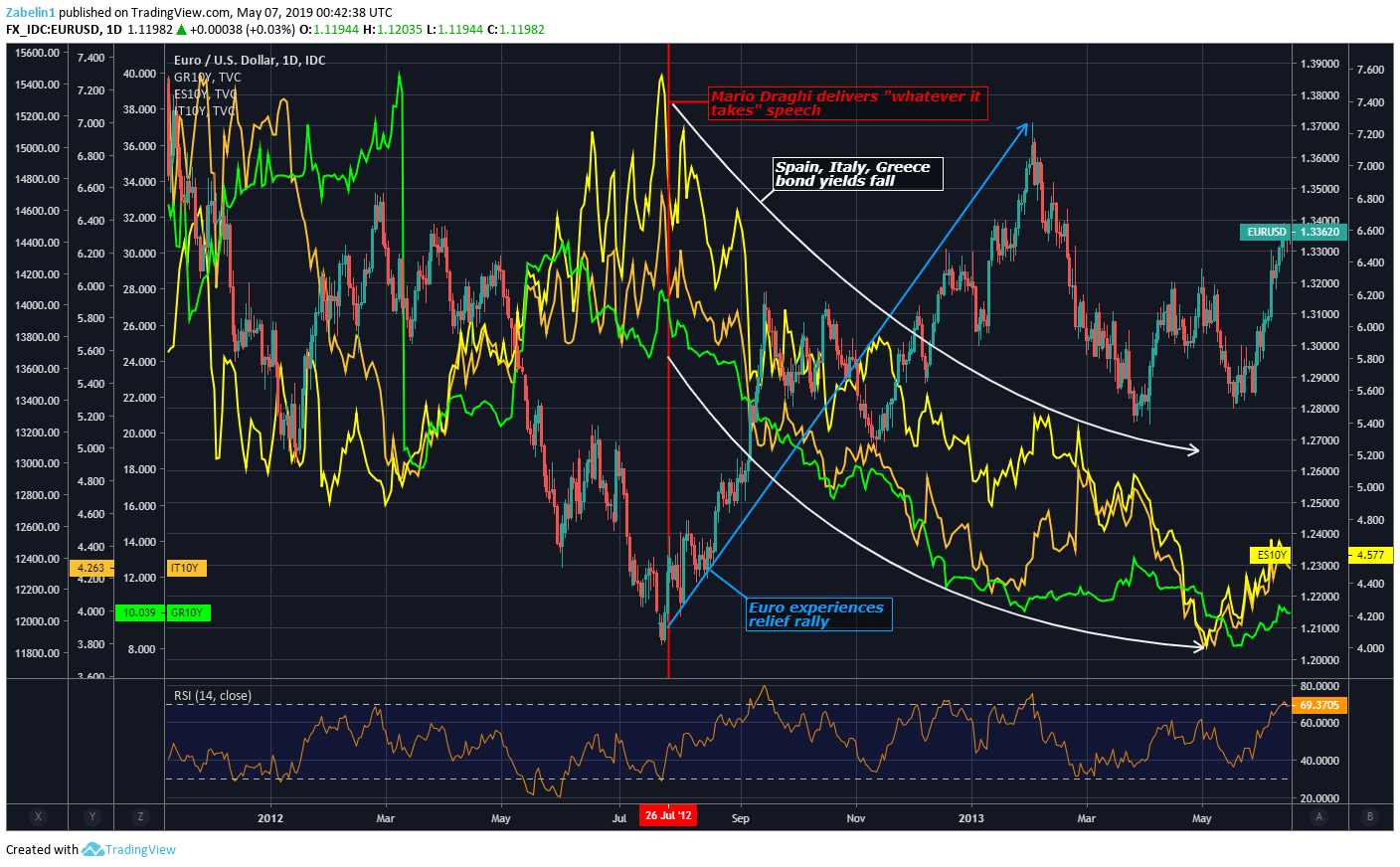

The 2008 global financial crisis and the ensuing Great Recession swept across the globe, destabilizing the Mediterranean region. That fueled fears of a regional sovereign debt crisis as bond yields in Italy, Spain and Greece climbed to worrisome levels. In some cases, mandatory austerity measures have been implemented, laying the groundwork for the Euroskeptic populism plaguing the region.

Investors are starting to lose confidence in the ability of these governments to service their debts and demand higher yields to take on what appears to be an increasing risk of default. If a crisis forces a member state to leave the euro zone in unprecedented ways, doubts will arise about the existence of the euro.

On July 26, 2012, Mario Draghi, President of the European Central Bank (ECB), spoke in London in one of the most iconic moments in financial history, seen by many as a bailout of the single currency. crucial moment. He said the ECB was “ready to do whatever it takes to protect the euro. Trust me,” he added, “it will work.” That speech calmed European bond markets and helped push yields lower.

Recommended by Dimitri Zabelin

Top Trading Courses

The ECB also created a bond-buying program called OMT (or Outright Currency Transaction). It should ease pressure on government bond markets and bring relief to troubled euro zone governments. Although OMT has never been used, its availability helps to calm nervous investors. At the same time, many troubled countries in the euro zone decided to implement austerity measures to stabilize public finances.

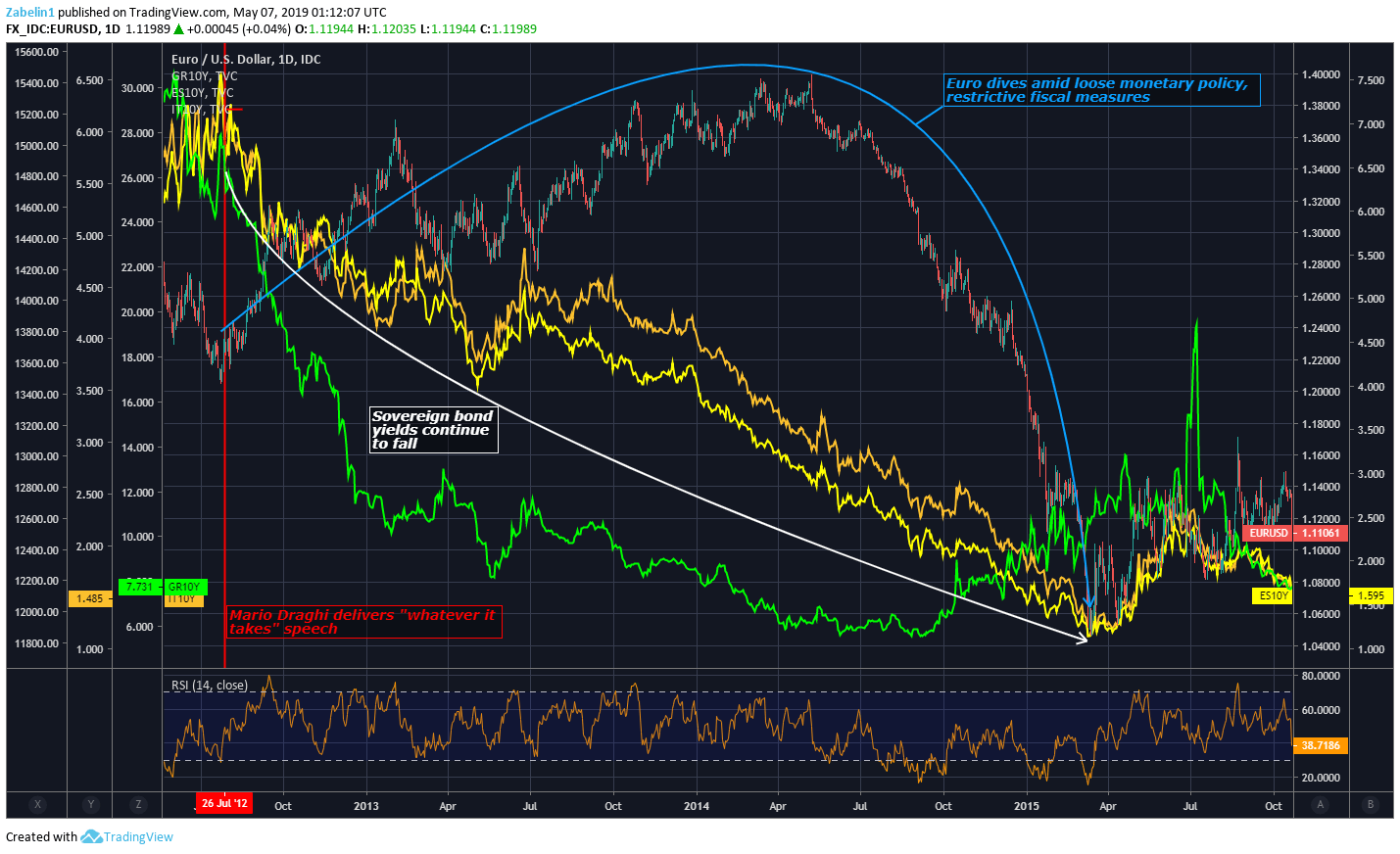

While the euro initially appreciated as fears of a collapse eased, the currency could depreciate sharply against the dollar over the next three years. By March 2015, it had lost more than 13% of its value. If you look at the monetary and fiscal structure, the reasons are obvious.

Scenario 2: Euro breathes a sigh of relief – government bond yields fall on heightened bankruptcy fears

Source: TradingView

Austerity measures in many euro zone countries have limited the ability of their governments to provide fiscal stimulus to help create jobs and boost inflation. Meanwhile, the central bank eased monetary policy to defuse the crisis. As a result, the combination pushed the euro lower against most major currencies.

Scenario 2: EUR and government bond yields fall

Source: TradingView

Scenario 3 – MONETARY POLICY LOOSE; FISCAL POLICY BECOMES TIGHTER

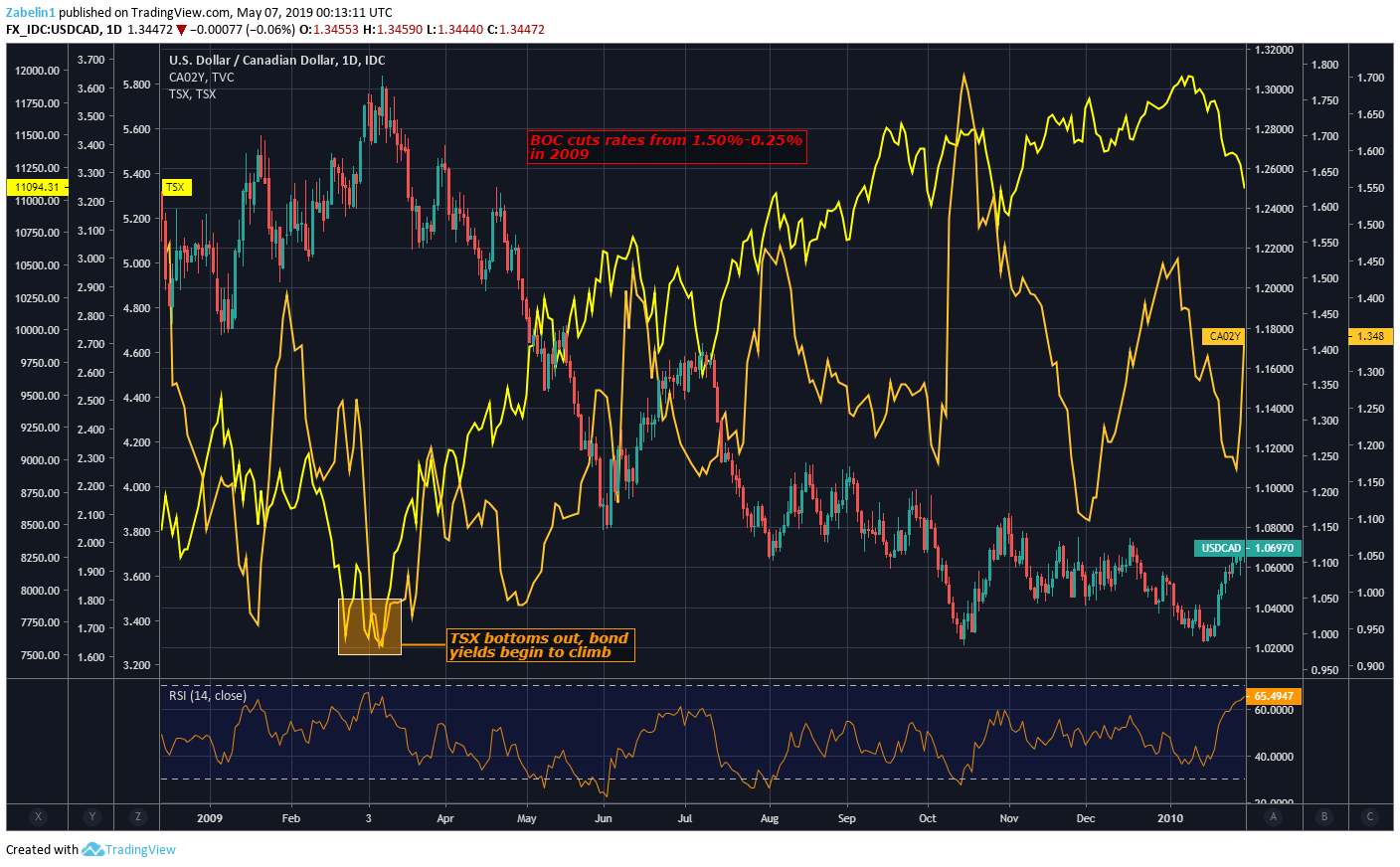

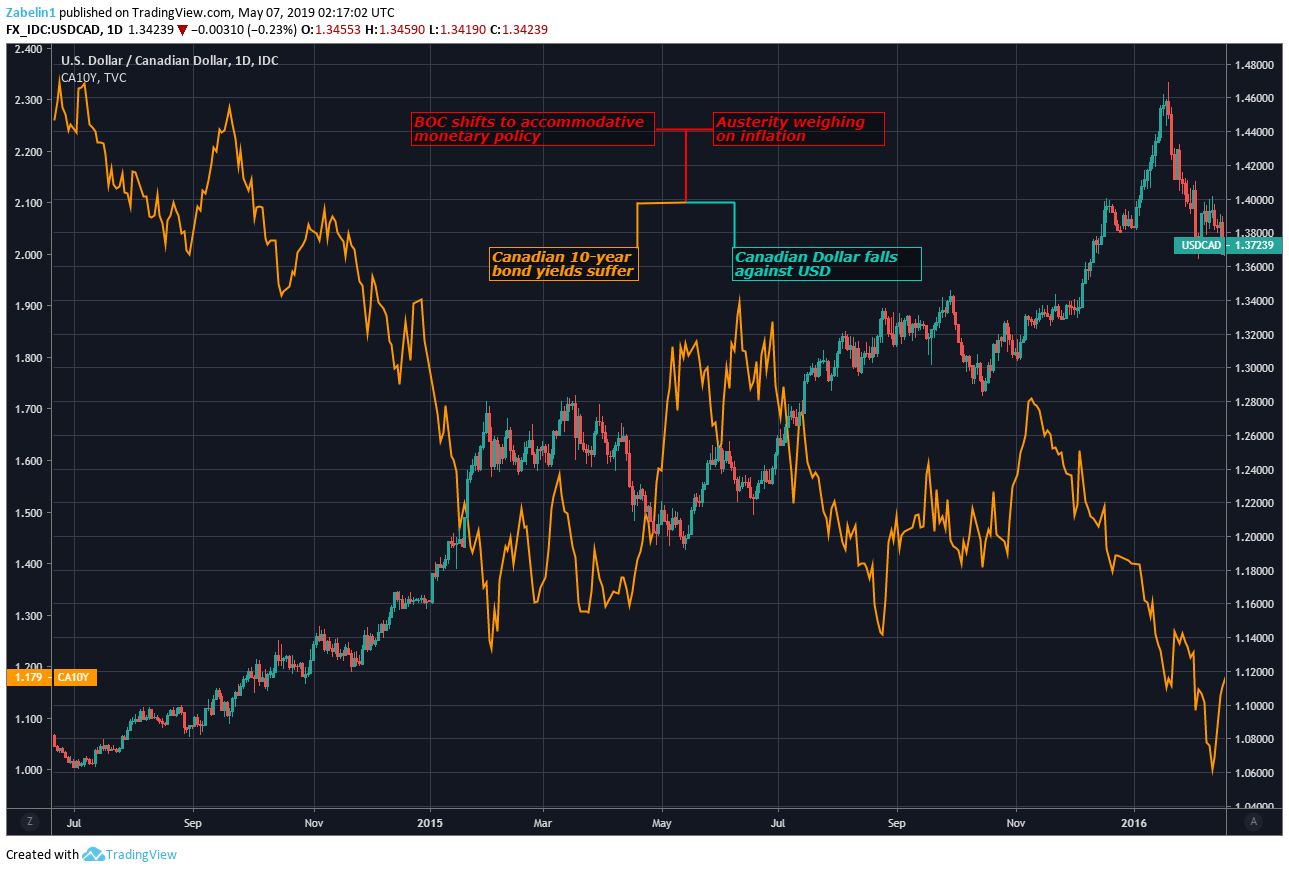

In the early stages of the Great Recession, the Bank of Canada (BOC) cut its benchmark interest rate from 1.50% to 0.25% in an effort to ease lending conditions, restore confidence and revive economic growth. Contrary to expectations, the yield on the Canadian government’s 10-year bond started to rise. The rally came as Canada’s benchmark TSX bottomed.

Scenario 3: USD/CAD, TSX, Canadian 2-year bond yields

Source: TradingView

The subsequent rebound in confidence and share prices was reflected in investor interest in higher-yielding, riskier assets such as stocks rather than relatively safe alternatives such as bonds. This reallocation of capital has resulted in higher yields despite central bank easing. The Bank of China then started raising interest rates again, taking them to 1% and keeping them there for the next five years.

During this period, Prime Minister Stephen Harper implemented austerity measures to stabilize government finances amid the global financial crisis. The central bank then reversed course, cutting interest rates to 0.50% by July 2015.

Both the Canadian dollar and local bond yields were affected by monetary easing and limited fiscal support capacity. Coincidentally, government spending cuts cost Mr Harper his job at this difficult time.

Scenario 3: USD/CAD, Canadian 2-year bond yield

Source: TradingView

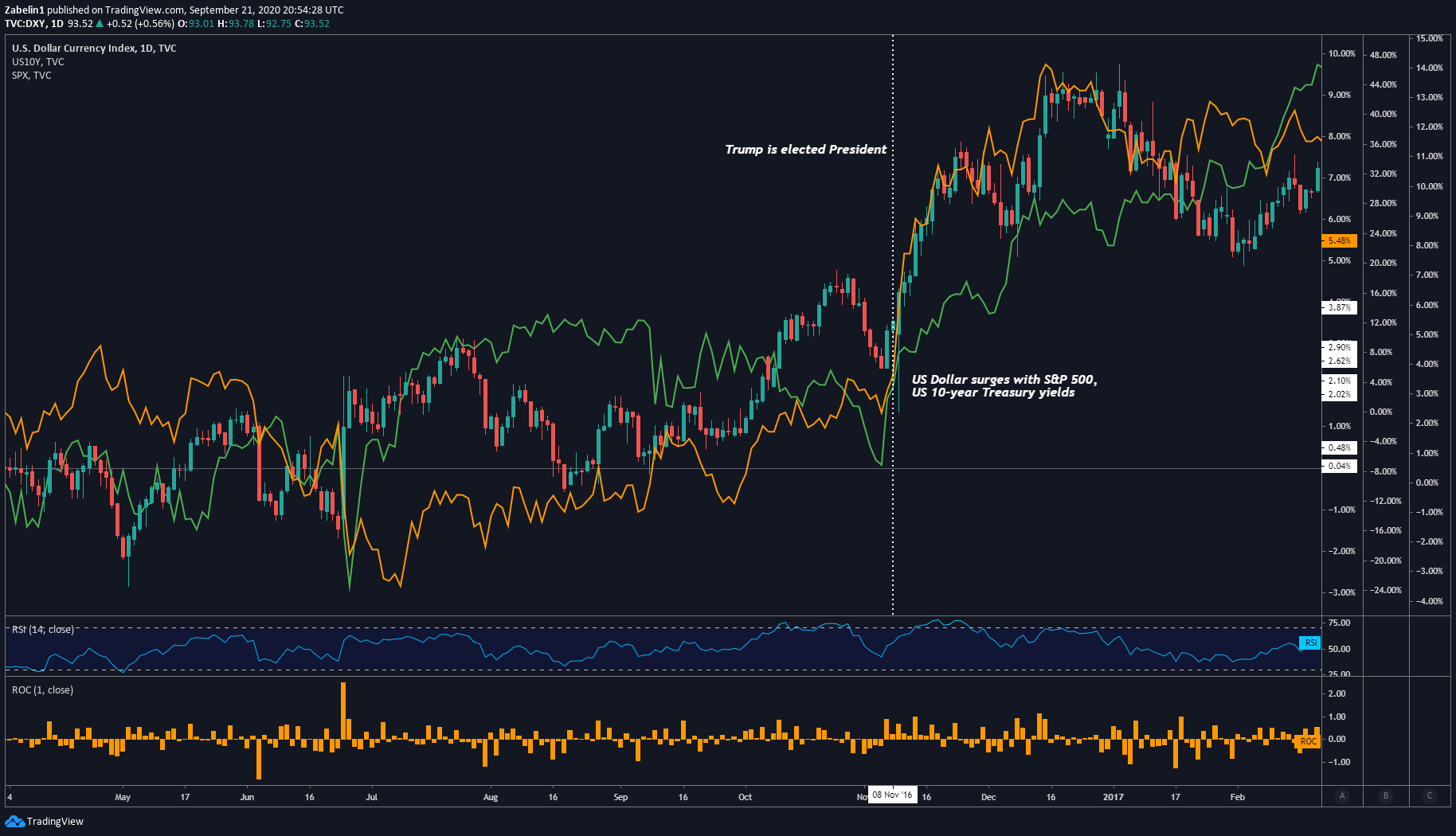

Scenario 4 – MONETARY POLICY TIGHT; FISCAL POLICY BECOMES LOOSER

The political landscape and economic backdrop favor a bullish outlook for the U.S. dollar after Donald Trump was declared the winner of the 2016 U.S. presidential election. With Republicans in control of the Oval Office and both houses of Congress, markets appear to be concluding that the room for political volatility has narrowed.

That makes market-friendly fiscal measures proposed by candidate Trump during his campaign more likely. These include tax cuts, deregulation and infrastructure development. At least for now, investors appear to be ignoring the threat of a trade war with major trading partners such as China and the euro zone. At the monetary level, central bank officials raised interest rates in late 2016, with the goal of raising rates further by at least 75 basis points by 2017.

The dollar rose alongside local bond yields and stocks as room for fiscal expansion and monetary tightening opened up.

Source: TradingView

WHY POLITICAL RISKS MATTER FOR TRADING

Numerous studies have shown that significant declines in living standards due to war or severe recession increase voters’ propensity to take radical positions on the political spectrum. As a result, people are more likely to deviate from pro-market policies—such as capital consolidation and trade liberalization—to focus on policies that deviate from globalization and are not conducive to inward-looking.

The modern globalized economy is politically and economically intertwined, so any systemic shock could have global effects. Monitoring these developments is critical during major political upheavals during intercontinental ideological shifts, as they provide opportunities for developing short-, medium- and long-term trade strategies.

[ad_2]