[ad_1]

Australian Dollar, AUD/USD, RBA, Fed, Recession, China – Talking Points

- AUD/USD weakens on global growth and mood swings

RBA admits inflation, but higher numbers may be in the pipeline

If the RBA is forced to raise interest rates, will this help or hinder AUD/USD?The Australian dollar is currently subject to volatility in risk appetite. A rebound in stocks late last week boosted the Aussie, but sentiment weakened earlier in the week.

Currencies linked to global growth are in a somewhat unique position. Growing fears of a U.S. recession as the Federal Reserve tries to rein in inflation has lowered growth prospects.

Tough policy tightening is needed to reduce annual headline inflation from 8.6% to the 2% target.

The U.S. has never lowered inflation by more than 2% without experiencing a recession. The problem appears to be the depth and duration of the slowdown.

Federal Reserve Chairman Jerome Powell stressed last week that the recession may not be as severe if supply chains ease. But if they don’t, the growth contraction can be painful.

A slowdown in the U.S. economy could complicate China’s post-pandemic economic recovery. China is a major buyer of Australian exports.

Amid recent optimism, Chinese stocks have been boosted over the past week by some good news about Shanghai reopening after lockdown.

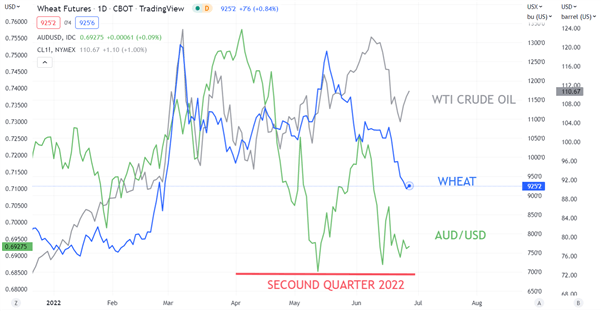

This is in stark contrast to price action in base metals, where tin and copper prices have fallen more than 20% from their recent highs. Iron ore is also weakening. The metals were affected by concerns about China’s growth prospects.

Australia’s trade balance has risen by about $10 billion a month due to the war in Ukraine, which has pushed up the prices of many of Australia’s exports. It remains to be seen whether the situation can be maintained.

Against this backdrop, the RBA has joined other central banks in implementing a robust tightening regime. Last week, RBA Governor Philip Lowe sounded the alarm on inflation and interest rates. The bank estimates the annual CPI in December to be around 7% and the cash rate is likely to be 2.5%. It is currently 0.85%. If we break down the CPI data, 7% inflation could come earlier than December.

The CPI for the second quarter of 2021 is 0.8%, which will be lower than the CPI due on July 27. The CPI for the first quarter of 2022 was 2.1%.

The first 3 months of the year, including only 1 month, saw sharp increases in commodity prices, especially energy and food prices. The biggest increase in production costs has yet to be fully passed on to consumers.

If we assume that the CPI for the second quarter of 2022 arrives at the same pace (2.1%) as the first quarter, the annual figure is 6.3%.

Given the unusual surge in energy, food and building materials in the second quarter of this year, higher numbers are likely.

The question remains, will a more hawkish RBA boost the Aussie?

[ad_2]