[ad_1]

Q2 2022 as expected in key trading opportunities in 2Q’22: US S&P 500 continues to outperform US NASDAQ 100; EUR/USD crosses March 2020 pandemic low of 1.0636 ; The U.S. Treasury yield curve (2s10s) entered inversion territory. More central banks are starting to hike rates aggressively, while fiscal stimulus is nowhere in sight.

However, factors that underscore the drivers of price action in Q1 2022 and Q2 22 may already be on track. As the Fed becomes more aggressive in raising rates, the odds of a Fed rate hike appear to have begun to change. Inflation expectations in advanced economies have stabilized, a sign that markets believe current cost of living growth is nearing the end of its upward trajectory. While the U.S. economy is likely to contract for a second straight quarter in 2Q222, supply chain disruptions and slowing growth in China may be less likely as China’s Covid-19 strategy emerges from excessive lockdowns; global growth should be in a slightly more volatile state good basis.

As for 3Q22, these factors point to a more optimistic period for global financial markets – even as economic data remains weak and sentiment remains subdued. Finally, the market tends to bottom before the economy, which will lead to cognitive dissonance among many market participants, especially new retailers.

CHINA NASDAQ GOLDEN DRAGON INDEX VERSUS US NASDAQ (ETF: HXC/QQQ) TECHNICAL ANALYSIS: DAILY CHART (January 2021 to June 2022)

As bad as U.S. stocks have been in 2022, Chinese stocks have fared much worse since the start of 2021. In the absence of an effective vaccine and draconian lockdown measures, China’s economy has had a disappointing performance over the past 18 months. But now, with China’s zero-coronavirus strategy from a total lockdown and Omicron’s dedicated vaccine on the horizon, the worst may be over for the Chinese stock market. The long HXC/short QQQ ratio is gradually moving higher on a six-month basis, suggesting that Chinese equities will outperform U.S. stocks for a while at least for the next few months. The ratio is likely to rise from around 28 to 36 in 3Q22.

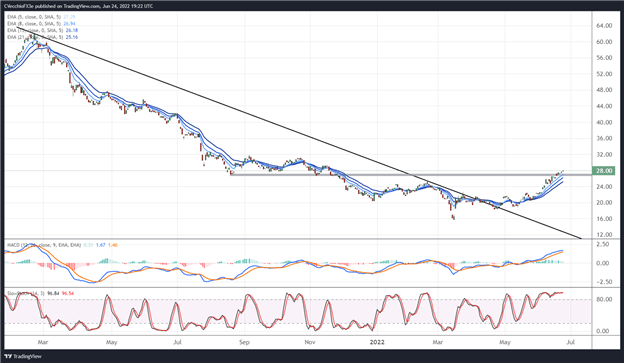

iSHARES BIOTECHNOLOGY (ETF: IBB) TECHNICAL ANALYSIS: DAILY CHART (June 2021 to June 2022) (CHART 2)

With inflation and growth concerns in the U.S. peaking, outdated industries — those that are cyclically sensitive — should fare better in the months ahead. One of the flagships of risk appetite in the U.S. stock market is the biotech sector, which has formed a double bottom over the past two months. Combined with a breakout of the downtrend from the September 2021, December 2021 and April 2022 highs, IBB could trade from 119.40 to 135.57 in 2Q22.

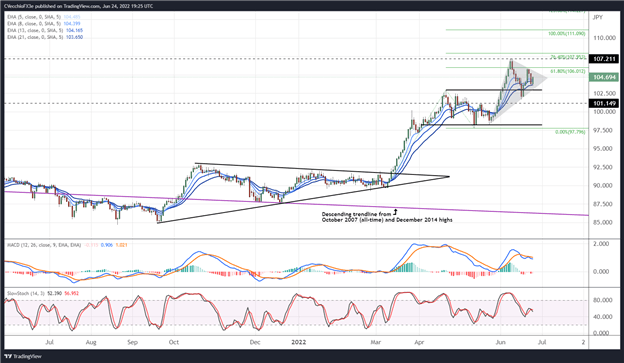

CAD/JPY TECHNICAL ANALYSIS: DAILY CHART (JUNE 2020 to JUNE 2022) (CHART 3)

The CAD/JPY pair has retreated over the past two weeks after breaking out of December 2014 highs, trading at levels not seen since February 2008. However, support was found at earlier resistance within the range starting in April 2022, suggesting that the technical stance remains bullish. The aforementioned range requires a measurable move higher above 108.00, but it hasn’t been taken yet, so there is a chance of further gains before exhaustion. A move back above the June high of 107.21 would provide a strong confirmation that the next move higher has begun, leading to a 100% Fibonacci of the March 2022 low/April 2022 high/May 2022 low Bonacci extension. 2022 low area at 111.09.

[ad_2]